Steve Sailer writes: A commenter replies to my latest Taki’s column proposing that all immigrants be required to have immigration insurance against any harms they may visit up Americans:

This is what I did for a living: design insurance and financial products. “Pittsburgh Thatcherite” has the kernel of brilliance but you have the wrong “bond”.

If you are talking about immigrant mass murders you have a low frequency high severity event.

One of my goals is to get the concept of liability for immigration on the table in the first place. Cigarette companies, for instance, always admitted they would be liable if, say, a cigarette exploded and burned your eyebrows off. But that got the lawyer’s nose in Camel’s tent: after lots and lots of arguing, it turned out the cigarette companies were also liable for increasing customers’ statistical risks of lung cancer. That process wouldn’t have been worth it if somebody with deep pockets wasn’t involved.

This makes an underwriter twitchy to begin with. You will never get meaningful limits in the context of such an event (yes, everyone buys car insurance and Mexicans get $15/30 limits) and insurers will be challenged to screen risks among the riskiest immigrants. The other obvious issue is that in a suretyship transaction there is an oligor (the immigrant) and oblige (his victims?) and a surety. The surety likes it when he is positioned to recover from the obligor after paying the obligee. Won’t happen here. This leaves out the question as to whether the surety/insurer is going to be penalized for underwriting by ethnicity.

This is a capital markets play. Some kind of immigrant CAT bond or quasi-CDS structure. This covers a generational cohort or some such number. The bond pays a premium if immigrants behave; maybe it pays a robust premium if immigrants reach certain socio-economic benchmarks. If Allah Akbar events spike, or socio-economic benchmarks crater, the bond pays no income and certain tranches risk their principal.

The reason this idea might work is that institutions could be shamed or pressured to issue the protection. Soros believes in immigration — hey, back it up. Maybe we could sell some of the bonds to Mexico. But any member of the pro-immigration elite could be made to pony up. Want HB-1 Visas? Buy the … bonds.

So if you want big limits — that are intrinsically diversified or pre-diversified — go to the capital markets not insurers. Another advantage: insurers deny claims. Swap counter-parties can’t. I believe AIG believed, in 2007, that it could weasel out of its CDS protection with Talmudic disputation (much like its D&O policies). AIG’s banks said: f you, we need another 10 billion in collateral for the market moving against you. The capital market clears.

Not immigrant insurance. Immigrant CAT bonds with different triggers and tranches, shoved down the throats of the elites cheerleading for more immigration.

Comments:

* That’s a great idea, but we also need to attach liability to judges, politicians and parole boards. These people can make policies or hand down rulings that will result in the deaths of citizens on a routine basis, but never face any consequences, except that politicians may not get elected again.

* The original insurance idea remains key for several reasons; this catastrophe (or “cat”) bond idea is really just footnote or ornamentation to it, but one with a certain amount of appeal I’ll grant.

To begin with, it is usually insurers, faced with risks on a mass of individual policies, who issue cat bonds for the purpose of laying off some of the correlated risks inherent in their portfolio of policies. If there is no insurer, which institution has an interest issuing the cat bonds to investors, and would bear the expense of paying back principal and interest if the immigrants behave, or retaining the principal if they don’t? The government? If there aren’t retail policies earning premiums, how does the bond issuer get income to support investment returns? If there aren’t claims against policies, to what use is the retained principal put if a trigger event occurs? Haven’t we already taken it as a given that the government just isn’t going to do a good job assessing immigration risk, which is why we need to bring in private institutions and litigants? Without underlying insurance policies, cat bonds don’t serve any particular purpose. When an underlying insurance market exists, cat bonds sometimes make sense as a way for an insurer to obtain reinsurance on the capital markets, as opposed to strictly through the institutional reinsurers and retrocessionaires, but cat bonds don’t really make sense in the absence of some kind of underlying exposure.

I admit, I do like the notion of publicly hoisting people by their own petards — forcing an amnesty advocate to put his money where his mouth is, requiring him invest his life savings in cat bonds issued by an insurer facing risks on a hundred thousand Syrian “refugees” — that would be a vintage Kodak moment.

The other subtle point is that cat bonds are most suitable for highly correlated, large, but infrequent risks — the kinds of concentrations that keep insurers (and their regulators) up at night. For example, car crashes are relatively small and fairly uncorrelated — plenty happen in a big city over the course of a year, but they all tend to happen in their own time for their own reasons. No one event brings about a devastating wave of car wrecks and losses (a good winter storm can bring about a brief spike, but relative to the number of wrecks in a year it won’t be significant), and year-to-year the numbers don’t change much. You don’t see cat bonds for car insurance risks. But windstorm losses can be very concentrated and correlated. Years can go by with few claims out of the East and Gulf Coasts. Then one day Hurricane Andrew or Katrina or Sandy rolls ashore and the industry is faced with tens of billions worth of insured losses in a day. Or years go by without major earthquake claims in California, but then one day Northridge happens. So you see cat bonds for earthquakes and windstorms.

All that being said, it would be interesting to see what types of cat bonds would or would not get issued in immigration insurance, and how they were priced on the capital markets. An insurer covering a large cohort of Syrian “refugees” — maybe that company issues a cat bond against terrorism risk and the next 9/11. Another carrier covering mainly Latin American agricultural workers — they don’t bother, because they’re mainly faced with small, uncorrelated traffic and petty-crime risks. Pricing information on individual policies is not always very transparent, but a cat bond quoted over the Bloomberg terminal would say a lot about human nature.

Finally, the tort litigation angle is brilliant and should not be underrated. Abstruse triggers on abstract financial instruments don’t make headlines. But had there been a million dollar liability policy on Francisco Sanchez, the illegal Mexican immigrant who shot Kathryn Steinle on a tourist pier in San Francisco, you’d get a whole extra layer of drama and headlines and attention. And I see your additional point — Steinle already made the papers. Having million dollar policies all over the place would encourage tort lawyers to dig up cases we’d never otherwise hear of, which has a huge value of its own.

* Another idea, staying with the original insurance scenario, would be to make the immigrant’s home country the obligor (or, in the cases of failed states, the UN). Then the insurer would have someone to recover from, and countries would have an incentive to police their emigrants.

* As I read that, I have a mental image in my head.

I see GOP as a big old dying tree. Most branches are barren of leaves. It’s been axed from all sides by Neocons, religious right dummies, globalist free traders, cuckservatives, crunchy cons, libertarian amoralists, and etc. There are huge chunks missing from the side. Few remaining fruits are picked just for the elites. It is about to fall over.

Then, Trump comes along and picks up an ax…

and everyone says HE is the one who destroyed the GOP.

Or imagine a dead man in a coffin nailed shut… but there’s one remaining nail. Trump picks it up and he is blamed for the death of the man.

Trump is no hero, and he may indeed bring about the implosion of the GOP, but the reason why so many have flocked to him is because GOP elites and politicians have been such wusses who never did anything to stop the globo agenda.

* One reason there are many Syrian emigrants right now is that they are fleeing massive American bombing. The Washington Post reported that the US has dropped more bombs (22,478) on Syria this year than the past five years in Afghanistan. This is all part of a failed four-year American attempt to overthrow the government of Syria.

Since the American people refuse to rein in such behavior by its leadership, and many of them condone or support such behavior, then obviously they’re liable for producing these emigrants, millions of whom are fleeing to neighboring countries and Europe.

* I’m afraid that if this idea ever gets off the ground, the gov and the media will work harder than ever to cover up perps’ identities and motivations.

Case in point, remember that incident at UC Merced a couple months ago? Every time I check back, it gets more interesting.

* Every citizen is given an annual immigration allotment, say 1,000th of one immigrant. Citizens can pool their allotments to bring in an immigrant and here’s the important part, they’re jointly and severally responsible for the good conduct and any damages caused by the immigrants and the next generation.

Having 1,000 people jointly and severally on the hook gives lawyers many targets to pillage.

* Admitting an immigrant is having someone join the American family. Immigrants should only be admitted in small numbers and after very careful vetting. The criteria should be based on how they benefit US society. That way we don’t have to worry about immigrants’ behavior once they are admitted.

As Derbyshire says, “maximum security at the borders and maximum liberty within the borders.”

* I think the focus should be on cutting off immigration completely or dramatically cutting back on the numbers we admit each year. The problem I have with the insurance proposal or any similar proposal is the propensity of the Democrats in Congress to seize on good sound Republican ideas and turn them into gold plated entitlements. That’s what happened to the sound, modest Republican plan back in the late 80′s to provide “catastrophic coverage” to Medicare recipients. By the time the Democrats finished adding their extensive little options, the plan’s cost had been dramatically increased, and the old folks rebelled. The chairman of the House Ways and Means Committee, Dan Rostenkowski of Chicago, was trapped in his limo by a mob of enraged octogenarians protesting the outrage. The old folks didn’t mind the added coverage. They just didn’t like the idea they were going to pay for it. Somebody else should pay for it. Obamacare was based on an idea originated by Republicans, and look what it turned into. What I fear happening is that the Democrats in Congress (they are eventually going to come back) will seize on the insurance proposal and twist it into an entitlement that gives each immigrant an extra thousand dollars a year to ease their transition into American life. So that, instead of saving American taxpayers money, the plan will cost them more and do noting to stem the flood of immigrants.

* How about the Swiss system: leave naturalization up to the municipal parliament, or in some cases, a local popular vote. Devolve decision making over immigration, as much as possible, to the local citizens affected by it.

Much of the extraordinary political friction over immigration comes from stakeholder disenfranchisement – the inability of citizens to influence decision making that directly impacts their neighborhoods. Immigration outcomes are felt, correctly, to reflect a democratic deficit. The effects of immigration take place in neighborhoods and municipalities, but the Feds/central government gets to regulate it. Maybe they shouldn’t.

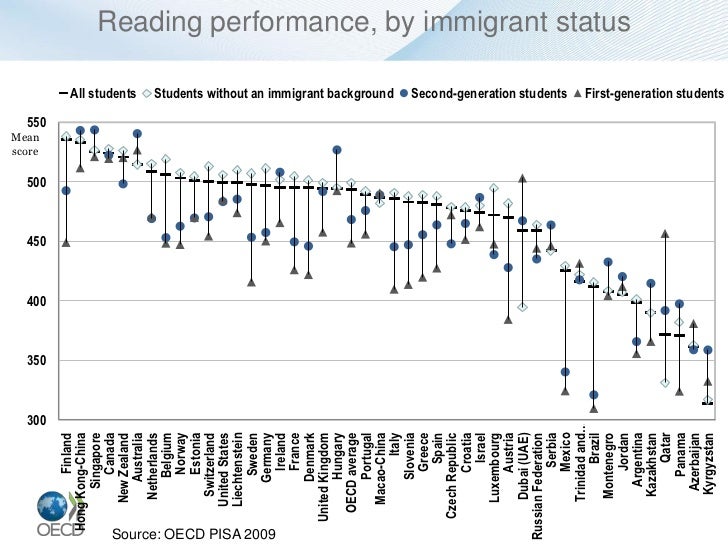

* Here’s a chart from the OECD – “reading performance by immigrant status” and Canada’s 1st and 2nd generation school kids read at about the same level as native born Canadians. In Australia, the 1st and 2nd generation immigrant kids out-perform native Australian kids. In the US though there is a big gap between native kids and 1st and 2nd generation immigrant kids.

{kind=link}

The real story in that data is what is happening in the Nordic countries and Europe, but it does provide answers for your US-Canada-Australia focus – screening immigrants results in higher human capital levels as expressed in the performance of children in school.

The fact that this immigration screening doesn’t result in Canada and Australia economically out-performing the US doesn’t invalidate the results of improved human capital levels.

The question that falls out from this is what dead-weight is the US carrying as a result of the low human capital levels of most of its immigrants? How much higher would US per capital income be if not for the deadweight of its immigrants?

Your response focuses on all of the gap that the US has accumulated and posits that this is due to immigrants, rather than addressing how much of that gap has narrowed because of the immigrants.